Marketing companies are heavily correlated to the wider economy, a low growth, low inflation economic recovery has been detrimental to the sectors growth in recent years. However, most listed marketing companies have risen generally with the stock market over the past seven years. This post gives a brief overview of the and its constituents who share a number of key characteristics:

· The annual accounts are stuffed with debt, goodwill, intangibles and one off costs reflecting the buy and build strategy utilised by many companies with the sector.

· The annual accounts are written by people who write attractive copy for a living, mentioning no names there is a fair amount of bullshit floating around.

This peer to peer comparison features marketing companies, the majority of which are full service agencies, meaning they specialise in all forms of marketing. The purely digital agencies have been extracted; they currently tend to be smaller companies with a lower market cap. I have also extracted companies which tend to specialise in one area of marketing like TLA Worldwide (TLA:LON) who are a dedicated sports marketing agency and venue advertising companies like Space & People (SAL:LON).

· The annual accounts are stuffed with debt, goodwill, intangibles and one off costs reflecting the buy and build strategy utilised by many companies with the sector.

· The annual accounts are written by people who write attractive copy for a living, mentioning no names there is a fair amount of bullshit floating around.

This peer to peer comparison features marketing companies, the majority of which are full service agencies, meaning they specialise in all forms of marketing. The purely digital agencies have been extracted; they currently tend to be smaller companies with a lower market cap. I have also extracted companies which tend to specialise in one area of marketing like TLA Worldwide (TLA:LON) who are a dedicated sports marketing agency and venue advertising companies like Space & People (SAL:LON).

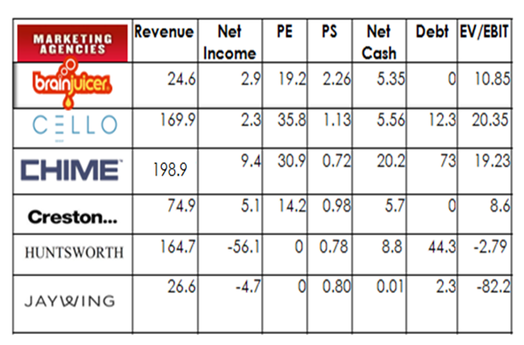

Brainjuicer (BJU:LON) has been highly profitable since listing in 2006 and had an eye-catching USP amongst peers. BJUs pitch is that turns human understanding into business knowledge. Judging by their testimonials their high profile clients seem to like the approach. The company has attained rapid growth and could benefit from a weaker pound with 36% of their revenue coming from outside the UK. The founder and chief executive John Kearon owns close to 32 per cent so is closely aligned to shareholders. Compare the cash conversion rates between BJU and Cello (CLL:LON) and you will see why BJU remains interesting. CLL meanwhile focuses on low margin work, the group has achieved a strong global position in the healthcare and digital marketing sectors. Recent results include nearly 6mn charges for restructuring, start-up losses, amortisation, remuneration/share option expenses, including a 2.1mn provision to resolve the VAT dispute with HMRC. Chime Communications (CHW:LON) have taken on debt in recent years to execute their buy and build strategy. The PE is high but reduces significantly for 2015/16, however, they have recently highlighted a mild profit warning for this financial year. As with many of their peers the balance sheet is negative by over 50mn.

Creston (CRE:LON) provided an update on trading for the year ended 31 March 2015 ahead of its preliminary results for the period, which are scheduled to be announced in June. Following a positive second half, CREs preliminary results for the period are expected to be in line with consensus.Revenue is expected to be £76.9 million (2014: £74.9 million).It has also announced the acquisition of How Splendid, which specialises in managing the digital user experience. The deal is expected to be earnings enhancing in FY16. Splendid brings in a high-quality client base across a broad range of verticals, including News UK, Boots and Barclaycard. CREs share price continues to reflect its past rather than its current position and prospects and the shares looks undervalued compared to its indebted peer group. Huntsworth (HNT:LON) has flat to falling in revenue with a significant level of debt which makes them a wholly unattractive proposition. I read recently that Matthew Freud has taken a sizeable position in HNT. Jaywing (JWNG:LON) were previously known as Weare2020 and have struggled to make a profit for several years now and have a wafer thin balance sheet.

Creston (CRE:LON) provided an update on trading for the year ended 31 March 2015 ahead of its preliminary results for the period, which are scheduled to be announced in June. Following a positive second half, CREs preliminary results for the period are expected to be in line with consensus.Revenue is expected to be £76.9 million (2014: £74.9 million).It has also announced the acquisition of How Splendid, which specialises in managing the digital user experience. The deal is expected to be earnings enhancing in FY16. Splendid brings in a high-quality client base across a broad range of verticals, including News UK, Boots and Barclaycard. CREs share price continues to reflect its past rather than its current position and prospects and the shares looks undervalued compared to its indebted peer group. Huntsworth (HNT:LON) has flat to falling in revenue with a significant level of debt which makes them a wholly unattractive proposition. I read recently that Matthew Freud has taken a sizeable position in HNT. Jaywing (JWNG:LON) were previously known as Weare2020 and have struggled to make a profit for several years now and have a wafer thin balance sheet.

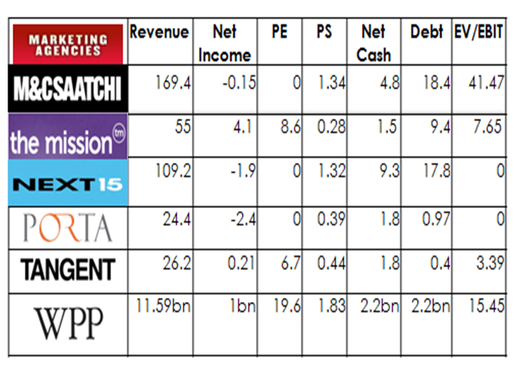

The M&C Saatchi (MAA:LON) name is synonymous with advertising and marketing and has a solid history and management. Recently they have taken on debt to diversify andhave just opened their first office in China. The FY14 accounts show many high profile client wins including Land Rover, John Lewis, Foot Locker and BMW. The balance sheet looks weak, again it’s stuffed with intangibles and there are some minority put options to consider. Overall an expanding company whose shares are overvalued. It may take a few years of rapid growth to develop a stronger balance sheet. Mission Marketing (TMMG:LON) offer a positive looking statement for the remainder of 2015, they also have one of the lowest PEs in the sector. It may be worth keeping an eye on this company to see if they achieve 2015s EPS figures. The real holdback here is the relatively high debt. Next Fifteen Communications (NFC:LON) are a fast growing marketing agency, their accounts are the most difficult to read, they have a ridiculous amount of income charts, dig below the headline profit and you’ll find debt and a weak balance sheet.

Porta Communications (PTCM:LON) looks like an interesting company with solid management who are attempting to build a diversified marketing group as they have done previously. PTCM was transformed by the year-end purchases of PPS and Publicasity which will not be included in its forthcoming results. The results sound interesting as management updated investors in February saying that revenue expected to be close to 30%higher than the previous financial year. They added that fee income expected to almost double and that there will be approximately 35% expected EBITDA growth. The results are released at the end of May and with manageable levels of debt, PTMN is well worth monitoring.Tangent Communications (TNG:LON) on the other hand is not, results have gone backwards in recent years and recent results have failed to halt the slide.

Finally we come on to the sector monolith, Sir Martin Sorrell’s WPP Group (WPP:LON) which acts as a barometer for the wider success of the sector. WPP is not cheap but you wouldnt expect the world’s largest advertising and marketing group to be cheap in an advanced bull market. Sir Martin Sorrell said his global advertising giant was on track to increase profitability by 0.3 points this year. Advertising and marketing are highly exposed to economic effects. Its share buyback programme should held the share price in the short term, whilst marketing spends slowly increase with world growth.

Disclosure: No position in any of the stocks mentioned

Porta Communications (PTCM:LON) looks like an interesting company with solid management who are attempting to build a diversified marketing group as they have done previously. PTCM was transformed by the year-end purchases of PPS and Publicasity which will not be included in its forthcoming results. The results sound interesting as management updated investors in February saying that revenue expected to be close to 30%higher than the previous financial year. They added that fee income expected to almost double and that there will be approximately 35% expected EBITDA growth. The results are released at the end of May and with manageable levels of debt, PTMN is well worth monitoring.Tangent Communications (TNG:LON) on the other hand is not, results have gone backwards in recent years and recent results have failed to halt the slide.

Finally we come on to the sector monolith, Sir Martin Sorrell’s WPP Group (WPP:LON) which acts as a barometer for the wider success of the sector. WPP is not cheap but you wouldnt expect the world’s largest advertising and marketing group to be cheap in an advanced bull market. Sir Martin Sorrell said his global advertising giant was on track to increase profitability by 0.3 points this year. Advertising and marketing are highly exposed to economic effects. Its share buyback programme should held the share price in the short term, whilst marketing spends slowly increase with world growth.

Disclosure: No position in any of the stocks mentioned

RSS Feed

RSS Feed