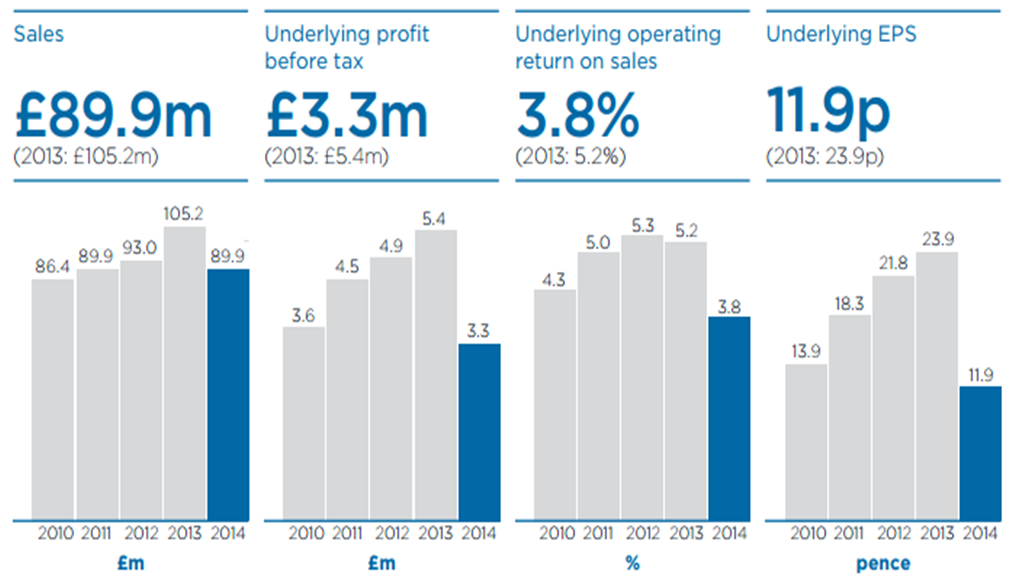

Currently at 75p MLIN trades at its lowest price for nearly four years at 4.8 times earnings and close to a 50% discount to the engineering sector. It’s net current assets currently exceed the market cap and the company suggests that it should comfortably meet current year expectations.

Molins had its beginnings in Cuba. Jose Molins began making cigars and hand-rolling cigarettes in Havana in 1874. After spending some time in America, he moved to London. In 1911 his two sons, Harold and Walter, devised a machine that could make a variety of packaging from cigarette packs to large cartons for tea. In July 1976 the company listed its shares on the London Stock Exchange.

Molins had its beginnings in Cuba. Jose Molins began making cigars and hand-rolling cigarettes in Havana in 1874. After spending some time in America, he moved to London. In 1911 his two sons, Harold and Walter, devised a machine that could make a variety of packaging from cigarette packs to large cartons for tea. In July 1976 the company listed its shares on the London Stock Exchange.

Molins is a technology-led service provider, with the tobacco industry accounting for around 45% of 2015 sales. 90% of revenues are derived from outside the UK, with a third coming from aftermarket services. FY14 was disappointing for MLIN. The Cerulean division was impacted by price competition from European rivals, who took advantage of the cheaper €euro. The tobacco division saw the industry close a number of large cigarette factories. The Asian tobacco market calmed and unrest in the Middle East has led to a general decline in some territories. However, the packaging divisions continued to grow driven by expansion in Asia, South America and a new customers across the pharmaceutical and healthcare industries.

Molins has a legacy pension deficit which I will look at in more detail later, however last year it fell from £15.2m to £9.7m, in line with higher investment returns. If we assume that the annual £1.8m per annum of payments are deducted from earnings, then the PE would climb from 4.8 to 7.3. Despite a testing year MLIN has kept the 7.3% dividend yield which is twice covered.

The majority of income is weighted towards the second half of the year and looking judging by the interims should be around the 14p level. Also mid year MLIN announced the sale of Arista Laboratories (details below), overall MLIN will make a small net loss on the sale, however Arista had been making consistent losses for the last few years.

Molins entered into an agreement with Enthalpy Analytical, Inc ('Enthalpy'), an affiliate of Montrose Environmental Group, Inc, for the sale of the trade and certain assets of its US based analytical services laboratory operation Arista Laboratories, Inc ("Arista"), for a consideration of $0.5m (£0.3m), which was paid in cash on completion. The sale represents the conclusion of the Company's strategic review of this operation which commenced in February 2015 as previously reported. In the year ended 31 December 2014 Arista generated revenues of £2.5m and incurred operating losses of £2.0m. The book value of its assets at 31 December 2014 was £2.8m. Enthalpy has assumed the obligations of the property lease of the premises from which Arista operates, the costs of which will be subsidised by the Group for a period of 18 months from completion, at a total cost of £0.4m payable in monthly amounts. The Group expects to incur a loss on this disposal of approximately £3.5m, of which £0.3m will be net cash payments, plus a £1.3m goodwill write-off.

Arista made a loss of £2.0mn in 2014, therefore this should considerably improve the bottom line. Now Arista has been jettisoned, the reporting structure has been simplified into two divisions - Packaging Machinery and Instrumentation & Tobacco Machinery. MLIN states that trading in the rest of the Scientific Services division is more challenging than expected, with tobacco sector conditions remaining difficult. The Packaging Machinery division, however, continues to trade ahead of last year and with Arista being treated as a discontinued operation in 2015, the Board expects the underlying trading performance of the Group for the year to be slightly ahead of current expectations.

From a high of just under £2.00 to a low of £50p MLIN does currently look cheap but the key in point from the interim statement for me is the trading slow down in the tobacco industry. My previous look at Karelia Tobacco shows that manufacturers and retailers are still making strong profits across the sector. There could be a number of possible reasons why MLIN is struggling in it's historic sector:

1 Increased competition from cheaper manufacturers from China and Asia?

2 Are monopolistic cigarette companies taking operations in house or squeezing the supply chain?

3 Is R&D from competitors translating into new disruptive technologies surpassing MLIN's systems?

The majority of income is weighted towards the second half of the year and looking judging by the interims should be around the 14p level. Also mid year MLIN announced the sale of Arista Laboratories (details below), overall MLIN will make a small net loss on the sale, however Arista had been making consistent losses for the last few years.

Molins entered into an agreement with Enthalpy Analytical, Inc ('Enthalpy'), an affiliate of Montrose Environmental Group, Inc, for the sale of the trade and certain assets of its US based analytical services laboratory operation Arista Laboratories, Inc ("Arista"), for a consideration of $0.5m (£0.3m), which was paid in cash on completion. The sale represents the conclusion of the Company's strategic review of this operation which commenced in February 2015 as previously reported. In the year ended 31 December 2014 Arista generated revenues of £2.5m and incurred operating losses of £2.0m. The book value of its assets at 31 December 2014 was £2.8m. Enthalpy has assumed the obligations of the property lease of the premises from which Arista operates, the costs of which will be subsidised by the Group for a period of 18 months from completion, at a total cost of £0.4m payable in monthly amounts. The Group expects to incur a loss on this disposal of approximately £3.5m, of which £0.3m will be net cash payments, plus a £1.3m goodwill write-off.

Arista made a loss of £2.0mn in 2014, therefore this should considerably improve the bottom line. Now Arista has been jettisoned, the reporting structure has been simplified into two divisions - Packaging Machinery and Instrumentation & Tobacco Machinery. MLIN states that trading in the rest of the Scientific Services division is more challenging than expected, with tobacco sector conditions remaining difficult. The Packaging Machinery division, however, continues to trade ahead of last year and with Arista being treated as a discontinued operation in 2015, the Board expects the underlying trading performance of the Group for the year to be slightly ahead of current expectations.

From a high of just under £2.00 to a low of £50p MLIN does currently look cheap but the key in point from the interim statement for me is the trading slow down in the tobacco industry. My previous look at Karelia Tobacco shows that manufacturers and retailers are still making strong profits across the sector. There could be a number of possible reasons why MLIN is struggling in it's historic sector:

1 Increased competition from cheaper manufacturers from China and Asia?

2 Are monopolistic cigarette companies taking operations in house or squeezing the supply chain?

3 Is R&D from competitors translating into new disruptive technologies surpassing MLIN's systems?

MLIN’s pension fund issues have been reported on for years it is a form of debt, and debt can correlate to share price. Looking closely at the asset breakdown of MLIN’s pension, it has a relatively high proportion of equities, around 60%, with current market returns MLIN should be close to the 6.4% assumed rate of return. Though the company achieved an average of 5-6% in the past few years I would argue that a 6% yield is above reasonable expectations.

The most recent statement on the deficit stated that:

The IAS 19 valuation of the UK scheme at 30 June 2015 shows a deficit of £7.6m (£6.1m net of deferred tax), compared with a deficit of £14.1m (£11.3m net of deferred tax) at the beginning of the period. The value of the scheme's assets at 30 June 2015 was £349.3m (31 December 2014: £347.9m), and the value of the scheme's liabilities decreased to £356.9m (31 December 2014: £362.0m). The net valuation of the USA pension schemes at 30 June 2015, with total assets of £14.6m, showed a reduced deficit of £6.0m (£3.6m net of deferred tax), compared with a deficit of £6.5m (£3.9m net of deferred tax) at the beginning of the period. The aggregate expense of administering the pension schemes was £0.4m (2014: £0.4m). The net financing expense on pension scheme balances was £0.4m (2014: £0.1m).

The UK scheme is subject to a formal triennial actuarial valuation as at 30 June 2015, with the deficit recovery plan being formally reassessed following its completion. The results of the last funding valuation, as at 30 June 2012, showed a funding level of 86% of liabilities, which represented a deficit of £53.0m. The level of deficit funding is £1.8m per annum (increasing by 2.1% per annum).

MLIN is a company in transition, moving into other sectors away from its traditional tobacco sector roots. Currently turnover is forecast to be in line with the same levels as 2011. At the moment I intend to watch how this plays out.

Disclosure: No position in MLIN

The most recent statement on the deficit stated that:

The IAS 19 valuation of the UK scheme at 30 June 2015 shows a deficit of £7.6m (£6.1m net of deferred tax), compared with a deficit of £14.1m (£11.3m net of deferred tax) at the beginning of the period. The value of the scheme's assets at 30 June 2015 was £349.3m (31 December 2014: £347.9m), and the value of the scheme's liabilities decreased to £356.9m (31 December 2014: £362.0m). The net valuation of the USA pension schemes at 30 June 2015, with total assets of £14.6m, showed a reduced deficit of £6.0m (£3.6m net of deferred tax), compared with a deficit of £6.5m (£3.9m net of deferred tax) at the beginning of the period. The aggregate expense of administering the pension schemes was £0.4m (2014: £0.4m). The net financing expense on pension scheme balances was £0.4m (2014: £0.1m).

The UK scheme is subject to a formal triennial actuarial valuation as at 30 June 2015, with the deficit recovery plan being formally reassessed following its completion. The results of the last funding valuation, as at 30 June 2012, showed a funding level of 86% of liabilities, which represented a deficit of £53.0m. The level of deficit funding is £1.8m per annum (increasing by 2.1% per annum).

MLIN is a company in transition, moving into other sectors away from its traditional tobacco sector roots. Currently turnover is forecast to be in line with the same levels as 2011. At the moment I intend to watch how this plays out.

Disclosure: No position in MLIN

RSS Feed

RSS Feed